What we do

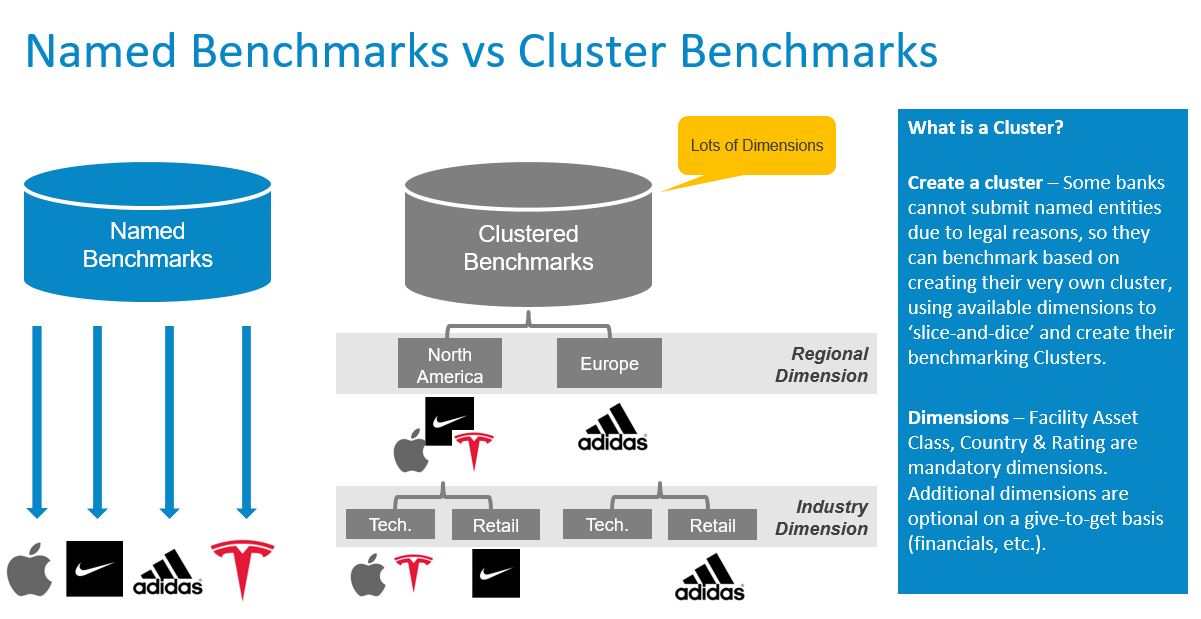

GCD benchmarking platform allows our members to benchmark the rating and loss estimates of their clients with those of their peers banks. Data exchange of the PD and LGD estimates on a name basis is performed in an anonymized way and treated with absolute confidentiality.

GCD has set up this service recently based on the wish of its member banks who have trusted GCD since years with their data handling and data security. The service offers data for more than 5000 clients worldwide as well as average PD and LGD levels for pre-defined clusters.

How can the database be embedded in your regular banking processes

- Directly benchmark your risk estimates (PD, LGD, EaD) on specific names and detailed risk clusters with your peers

- Follow changes in risk estimates over time

- Feedback the information in your model development and calibration processes