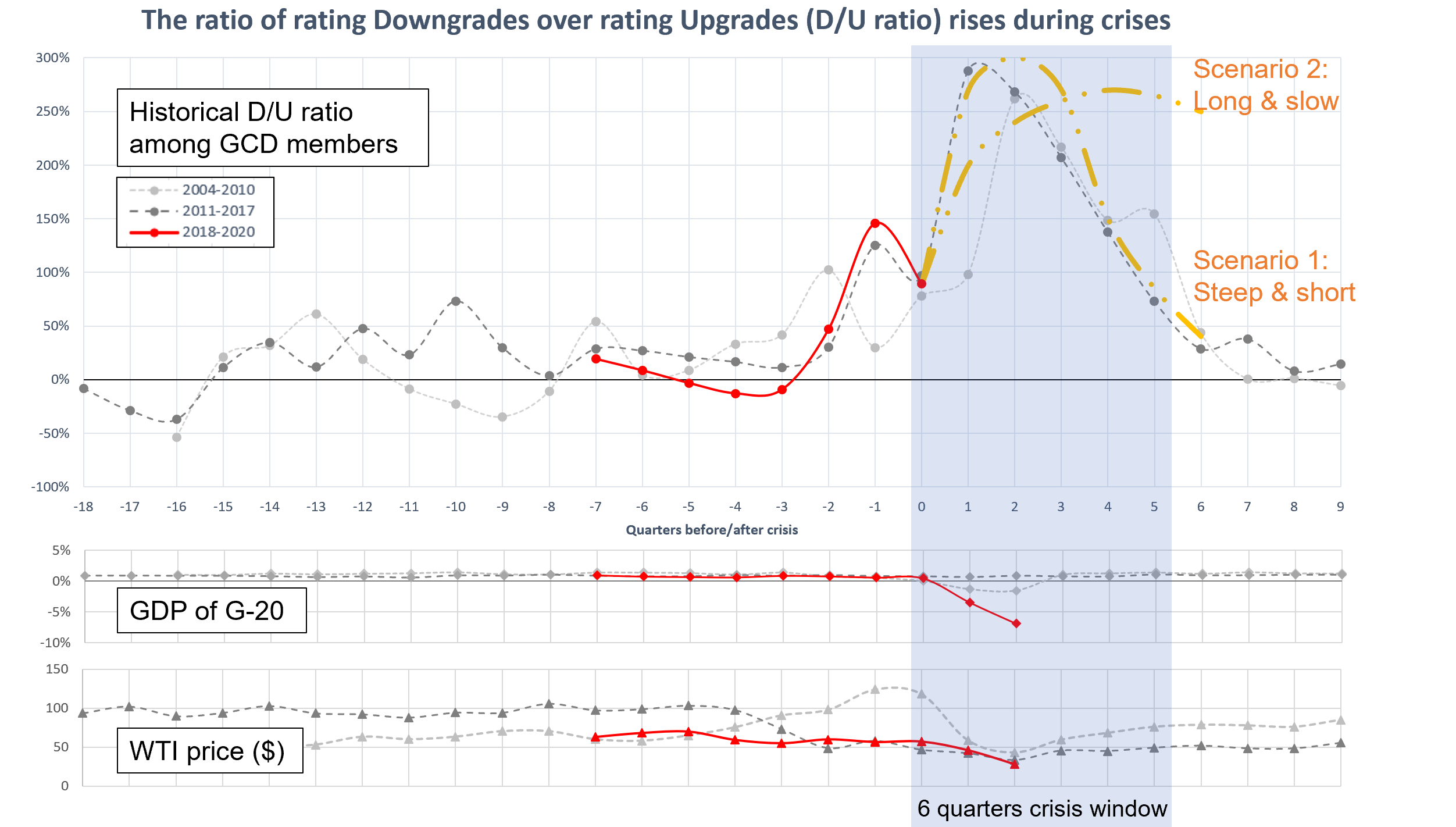

The D/U ratio is calculated as the count of rating downgrades over the count of rating upgrades for a lender during a specific period. It captures the assessment of banks’ risk profile, as they assess it with their internal ratings. As such, it is a forward-looking view on banks’ projections of the crisis.

Based on internal regulatory rating collection from GCD’s members banks, the D/U ratio is typically rising during crises. The pattern for these crises is very similar, which proves that historic data can indicate data-driven forecasts for crisis developments. The D/U ratio dynamic is strongly connected with relevant macroeconomic drivers.

In 2020, macroeconomic factors such as GDP and oil price, have already indicated their lowest historical performance for decades.

Find about the impact of the pandemic crisis on Rating Transitions

Join GCD banks benchmarking their portfolios and rating distributions shifts during 2020

With the economic impact of the COVID-19 pandemic continually and rapidly evolving, banks’ credit risk teams need to adjust their models in step. In order to do this, they need to have the most up-to-date and relevant data to hand.

To support the industry in understanding the impact of these events on PD and ratings, GCD is executing a special COVID-19 run of its PD and Rating Platform.

Objective:

To give banks’ credit risk teams timely insight into the impact of the COVID-19 pandemic on PD and ratings in relation to their peers.

How to participate:

- Contact Olivier Plaetevoet to register your interest

- Submit unaggregated data, including asset class, country/geographic region, industry, rating category and PD for Q4/2019, Q1/2020, Q2/2020, Q3/2020

What you get in return:

At a time where uncertainty abounds, this earlier-than-usual run offers participants timely information on the economic impact of the pandemic. This provides critical insights for banks’ credit risk teams, enabling them to adjust their models based on confidential, high-quality, granular and anonymous data.

With this database, banks can enhance the backtesting, calibration and benchmarking of their internal PD models. In addition, member banks can directly compare their level of calibration and model accuracy with peers to gain further insights into the overall performance of their models.

Some use cases include:

- Benchmark your PD masterscale

- Benchmark your system’s discriminatory power

- Identify macro-economic dependencies in default and migration data: extract a “systemic factor” from rating migrations or default rates

- Benchmark your asset correlations and long term default rates

- Benchmark your stage allocation / SICR buckets (thresholds for “lifetime PD” movements) under IFRS 9

- Reduce uncertainty add-ons for lack of data

If you are interested in learning more, contact Olivier Plaetevoet.

{kind=link}