- This event has passed.

North America Round Table: PD & Benchmarking

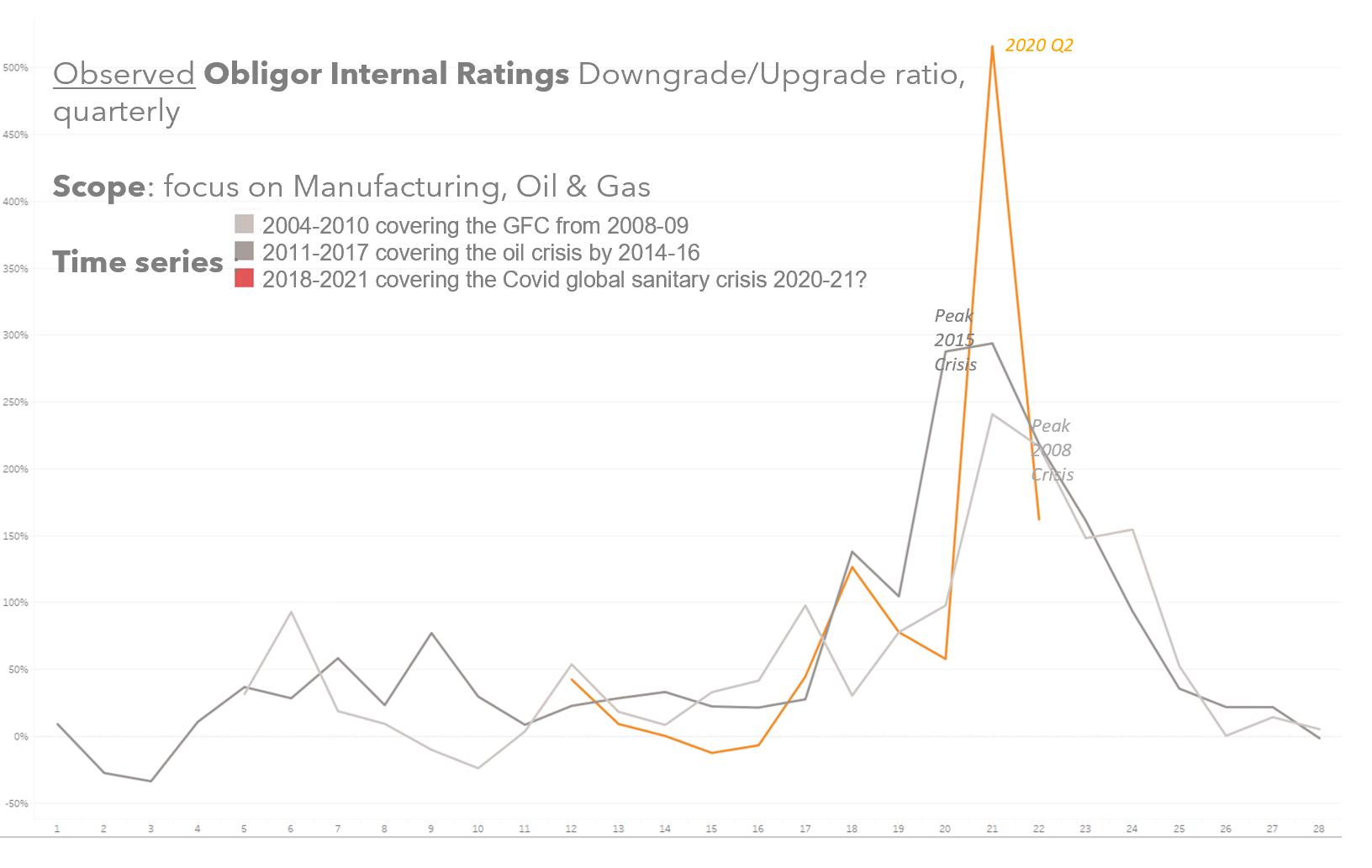

The Covid-19 pandemic had greatly affected many bank’s obligors, particularly in the United States.

In response, our member banks have had to re-grade many of their obligors and the patterns of change due to the pandemic can be seen in GCD’s PD databases.

At the interest of our member banks Global Credit Data will be having a roundtable discussion on the activity we’ve seen in our Probability of Default platforms.

We encourage all who are interested to attend this round table with our PD platform participating banks and join us in the discussion of these important developments.

This roundtable discussion will be held Monday February 22th at 1:00pm EST. The login information is also below.

Topic: GCD Probability of Default Roundtable

Time: Feb 22, 2021 01:00 PM Eastern Time (US and Canada)

Join Zoom Meeting

https://globalcreditdata.zoom.us/j/96684636161

Meeting ID: 966 8463 6161

One tap mobile

+19294362866,,96684636161# US (New York)

+13126266799,,96684636161# US (Chicago)

Dial by your location

+1 929 436 2866 US (New York)

+1 312 626 6799 US (Chicago)

+1 301 715 8592 US (Washington DC)

+1 346 248 7799 US (Houston)

+1 669 900 6833 US (San Jose)

+1 253 215 8782 US (Tacoma)

Meeting ID: 966 8463 6161

Find your local number: https://globalcreditdata.zoom.us/u/aWwkX2OL

Join by Skype for Business

https://globalcreditdata.zoom.us/skype/96684636161

Location:

Online