GCD Newsletter – March 2023

Read the March 2023 Newsletter here....

GCD Data Quality Dashboard 2023 – available

Since 2004, GCD has continuously reinforced a framework that is used to measure and monitor Data Quality (DQ). The objective is to achieve high DQ and compliance for the GCD pooled data, as required by global regulations (BCBS 239, ECB Guide to internal models, Fed...Global Credit Data Releases New Funds Peer Benchmarking Report Based on Extensive Industry Data

Global Credit Data, in collaboration with AFME, has published a new report providing empirical evidence on the risk profile of fund exposures under Basel 3.1. The analysis draws on a unique dataset of more than 40,000 funds collected from 13 banks, complemented by...

Federal Reserve references GCD Data in Supervisory Stress Test Model Documentation

Powered by data from World’s Leading Banks - Trusted by the Federal Reserve of US. Global Credit Data (GCD) is the premier global source for benchmarking defaults, losses, and recoveries on commercial loans. Backed by 50+ member banks worldwide, our non-profit...

GCD-developed industry standard to show pooled loss data is representative of banks’ portfolios

Banks seek EU supervisory green light on external credit data GCD-developed industry standard to show pooled loss data is representative of banks’ portfolios Click Here to read more: risk.net Download the GCD Representativeness...

New Report: Climate & Credit Risk – Benchmarking Report by UNEP FI & GCD

Current Approaches and Emerging Trends for Climate-Related Credit Risk Assessment Methodologies—insights from a global survey Download here: Climate & Credit Risk Report This report offers a detailed analysis of how banks currently assess and manage...

Results Released! Climate Risk Benchmarking Survey by GCD and UNEP FI

Climate Risk Benchmarking Results! UNEP FI and GCD recently completed a global survey assessing how banks are integrating climate risks into their credit risk frameworks. Covering methodologies, data sources, and scenario analysis across sectors, the results provide a...

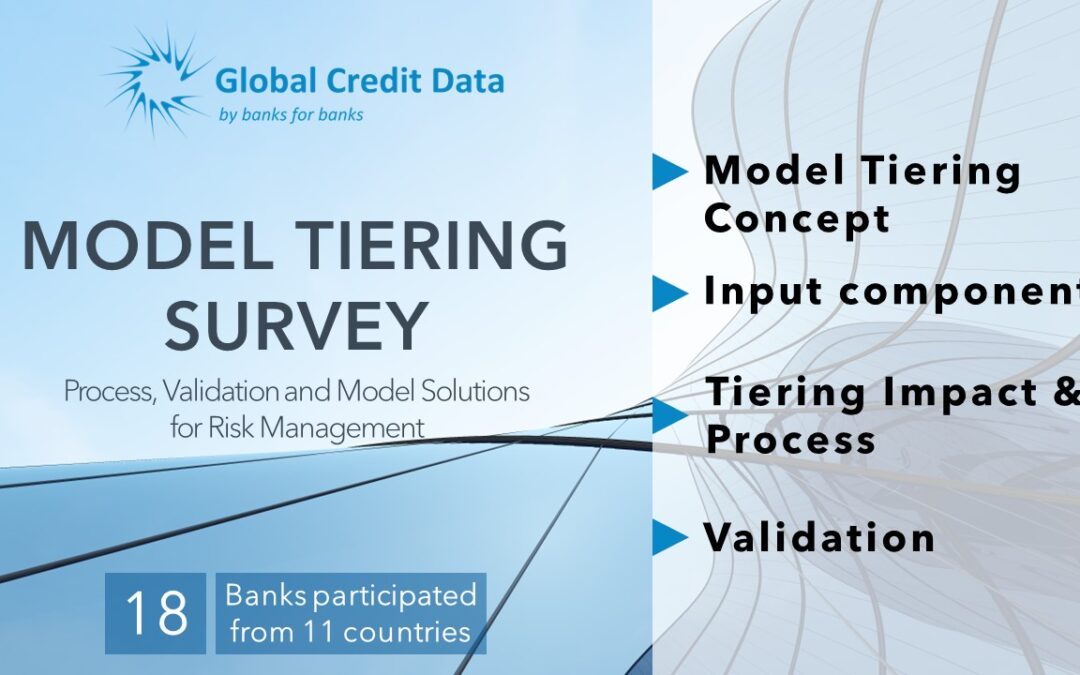

GCD Model Tiering Survey Results Released

Model Tiering Survey Model tiering refers to the classification of a model into a specific category of relevance for model risk management purpose.For example, such categories can be labelled “high relevance”, “medium relevance”, “low relevance”.This classification is...

Climate Risk Benchmarking Survey by GCD and UNEP FI – Registration Now Open!

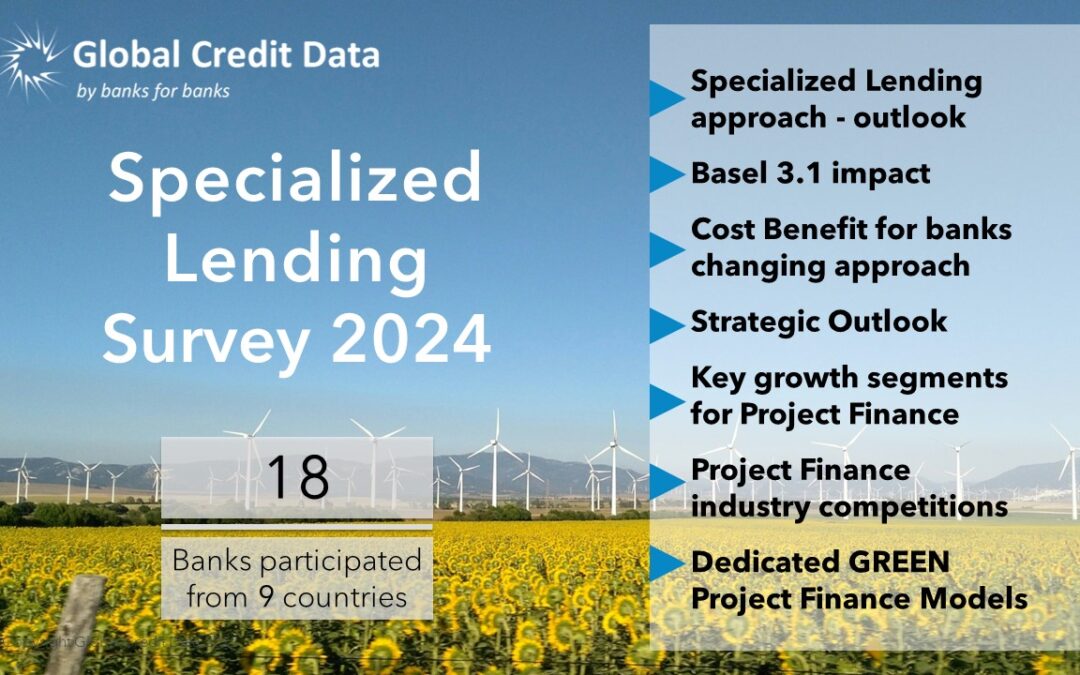

GCD Specialized Lending Survey 2024

Specialized Lending Survey Understanding and managing risks effectively requires robust data. This is especially challenging for low default portfolios like Specialised Lending, meaning banks often lack sufficient internal defaults for modeling. Also in the...

Pandemic Aftermath: GCD Data Reveals Decline in US Real Estate Recovery Rates

New Report Highlights Impact of COVID-19 on U.S. Commercial Real Estate Pandemic Aftermath: GCD Data Reveals Decline in US Real Estate Recovery Rates July 19, 2024 – GCD today announces the release of the "US Real Estate Recovery Rates Report - Sectoral Comparison of...